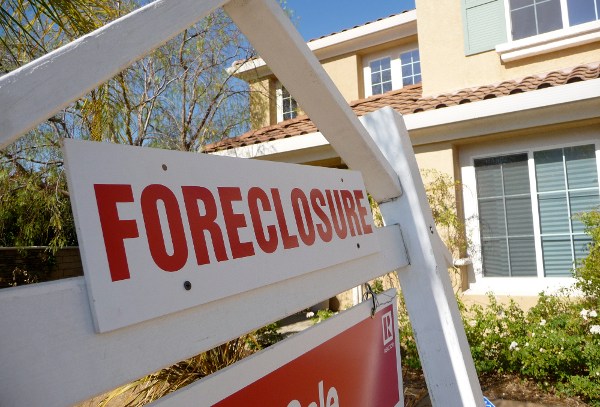

States Strike Back: CA Takes Action on Home Foreclosures

The California legislature passed a landmark bill Monday strongly regulating how banks handle home foreclosures. The legislation bans dual tracking, the odious practice where lenders pursue home foreclosure while negotiating with homeowners about modifying mortgage terms. Robo-signing-- falsifying signatures-- on mortgage documents is now illegal. The state and private citizens can now sue financial institutions for violating the law. Finally, loan servicers and banks must provide a single point of contact for clients.

These are badly needed regulations. Dual tracking too often was just a pretext. The loan servicer would pretend to be negotiating with the homeowner while instead focusing on foreclosure. That deceptive maneuver is now prohibited. Robo-signing, the deliberate use of fraudulent signatures in thousands of documents should have been and probably always was illegal. But the new California law makes it bluntly clear and mandates criminal penalties. That such a law needed to be spelled out so clearly simply shows how evasive, uncooperative, and sometimes criminal our financial institutions have been in the home foreclosure crisis.

Banks often do not want distressed properties to be sold or foreclosed. Through a number of quite legal transactions, they can transfer ownership to a subsidiary, sometimes by a deed in lieu of foreclosure:

"In general, banks have devised ways to perform financial alchemy," said Ken Thomas, a Miami economist and bank analyst. "They take a problem loan and, through different legal actions, turn it into a non-problem loan."

In the wake of the financial crisis, FASB suspended mark-to-market and allowed values based on cash flows, leading some to call such a practice “mark-to-fantasy” and “pretend and extend” because it doesn’t solve the underlying issues.

The California legislation, which has not yet been signed by Gov. Brown, makes this process more difficult for banks to do. Banks must either negotiate terms or foreclose. They cannot do both. Further, oversight has been increased, with penalties for dodgy behavior.

Many other states are considering tougher mortgage regulation too, a process strongly resisted by banks who say it will raise costs for all:

"Should all 50 states decide to go down their own path, lenders are going to have multiple processes, each with their own little nuances, and every single penny of that cost will be borne by tomorrow's borrowers," said David Stevens, chief executive of the Mortgage Bankers Association.

But the individual states already have individual laws on mortgages and costs are often absorbed by corporations in order to remain competitive. So this is really a non-argument.

Our entire financial system is in need of reform. The California mortgage reform bill is an important first step.

Latest articles